When you receive your salary, it is not just a fixed amount credited to your account. It is divided into different parts like basic pay, allowances, and other benefits. Many companies today also include flexible components in the salary structure to give employees more control over how their income is used.

One such component is FBP, which often confuses employees because it involves choices, declarations, and reimbursements. If not understood properly, you might miss out on valuable tax-saving opportunities or end up selecting options that don’t actually benefit you.

Understanding how FBP in salary works is important if you want to make smarter financial decisions and improve your net salary. This blog will guide you through everything in simple and easy-to-understand language, so even if you are new to salary structures, you can follow along without any confusion.

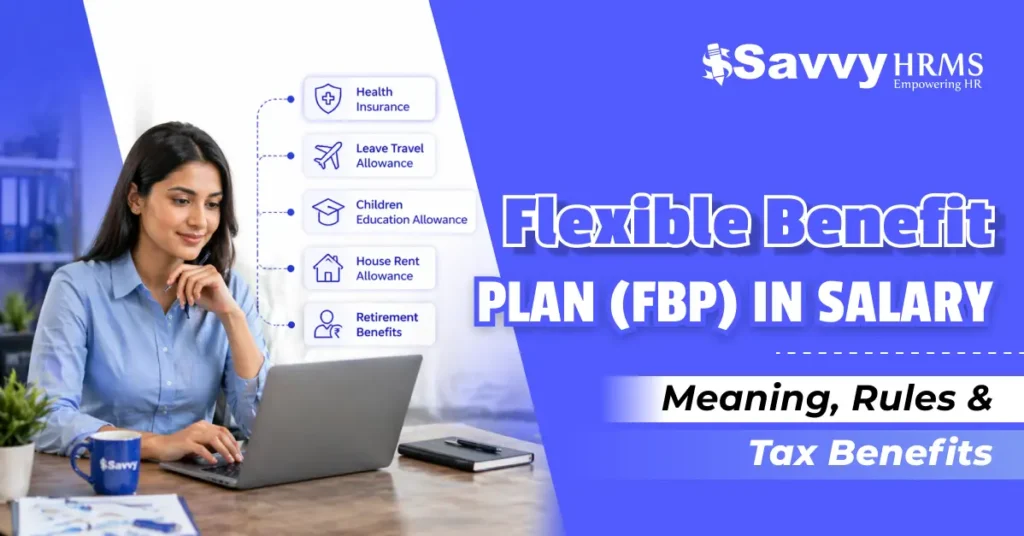

FBP Full Form and Meaning in Salary

The FBP full form is Flexible Benefit Plan.

It is a part of your salary that gives you the freedom to choose how some portion of your salary is used, based on your personal needs and expenses.

Simple Meaning of FBP

In a normal salary, everything is fixed. But with FBP, you get flexibility.

You can customize your salary structure by selecting benefits such as:

- Food or meal allowance

- Travel or conveyance expenses

- Mobile and internet bills

- Fuel or car expenses

Instead of receiving this amount as a fully taxable salary, you can claim it as reimbursement, which helps you:

- Pay less tax

- Get a higher net

How Flexible Benefit Plan (FBP) Works in CTC?

Your CTC (Cost to Company) is your total salary package. A part of this salary is set aside as FBP (Flexible Benefit Plan).

This means:

- You don’t get this amount directly as cash

- Instead, you can use it for specific expenses and save tax

Example to Understand Easily

Suppose your total CTC is ₹6,00,000 per year

Out of this:

₹1,00,000 is allocated as FBP

Now, you can decide how to use this ₹1,00,000 based on your needs.

For example:

- ₹20,000 for food expenses

- ₹30,000 for fuel or travel

- ₹50,000 for other reimbursements (like phone bills, books, etc.)

You will get tax benefits only if you actually spend this money and submit proof.

That means:

- Keep your bills (receipts, invoices)

- Upload them in your company portal

- Claim reimbursements

If you don’t submit proofs, this amount may become fully taxable, just like your regular salary.

What is Flexible Benefit Plan (FBP) Declaration?

FBP declaration means choosing how you want to use the flexible part of your salary.

In simple words:

It’s when you tell your company:

“I want to use my FBP for things like food, fuel, or phone bills.”

Example:

If you have ₹1,00,000 FBP, you can decide:

- ₹30,000 for fuel

- ₹20,000 for food

- ₹50,000 for other expenses

That choice is your FBP declaration.

Common Flexible Benefit Plan (FBP) components that people usually see

| Component | What it means in simple words | Key tax note |

| House Rent Allowance | If you live in rented accommodation, HRA can reduce tax under the old-style salary exemption rules. | Official exemption is the least of actual HRA received, rent minus 10% of salary, or 40% of salary, rising to 50% in Mumbai, Kolkata, Delhi, and Chennai. HRA exemption is not available in the new tax regime. |

| Leave Travel Allowance | Travel support for leave trips taken in India. | Officially linked to travel fare within India, generally available for two journeys in a block of four years, subject to the prescribed fare limits and proof. |

| Telephone or mobile expenses | Work-related mobile or communication expenses paid by the employer. | Official guidance says employer-paid telephone and mobile facility is not treated as a taxable perquisite in the normal sense. |

| Conveyance for official duties | Travel expense while doing your work, not simply traveling from home to office. | Official guidance treats conveyance allowance for performance of duties as exempt to the extent of expenditure incurred. That is different from ordinary daily commuting. |

| Children’s education and hostel allowance | Small allowances for children’s education or hostel costs. | The official AY 2026-27 benefits guide lists ₹100 per month per child for up to two children for education allowance and ₹300 per month per child for up to two children for hostel expenditure allowance. |

| Uniform or academic allowance | Support for uniforms or approved academic/research or training-related spend. | Official guidance allows uniform and research/academic allowance relief to the extent of actual expenditure incurred, where the relevant conditions are met. |

Types of Flexible Benefit Plan (FBP) Policies

Companies design FBP policies in different ways to balance flexibility for employees and control for the organization. Understanding these policies helps you make smarter choices and maximize your tax benefits.

1. Quantity-Based Policy

In this policy, the company assigns a fixed limit to each benefit category, and you can claim expenses only within that limit.

Example:

- Fuel allowance: ₹20,000 per year

- Phone bills: ₹15,000 per year

Even if your actual spending is higher, the reimbursement is capped at the predefined amount.

2. Opt-In Policy

This policy allows employees to select benefits based on their personal needs at the beginning of the financial year.

Example:

- If you rarely travel, you can skip conveyance allowance

- You can allocate more to internet, food, or learning expenses

Another Example:

- An employee working from home may choose higher internet reimbursement and skip fuel expenses

You actively choose (“opt in”) the benefits you want to include in your salary.

3. Mutual Exclusion Policy

In this policy, certain benefits are interconnected, and selecting one will automatically exclude another related benefit.

Example:

- If you choose a company-leased car, you may not be eligible for fuel reimbursement separately

Another Example:

- If you opt for a company-provided accommodation, you may not be allowed to claim house rent allowance (HRA)

This ensures that employees don’t claim multiple benefits for the same purpose.

Advantages of Flexible Benefit Plan (FBP)

A Flexible Benefit Plan is not just a salary component. It is a smart way to optimize your income, reduce taxes, and manage everyday expenses efficiently. When used correctly, it can make a noticeable difference in your overall earnings.

For Employees

1. Significant tax savings

FBP allows you to convert a part of your taxable salary into reimbursements. For example, instead of paying full tax on ₹20,000, you can claim it under fuel or phone bills and reduce your tax liability.

2. Higher take-home salary every month

Since a portion of your salary becomes tax-exempt, your in-hand salary increases without any hike in CTC.

3. Salary tailored to your lifestyle

If you travel more, you can allocate more towards fuel. If you work remotely, you can use it for internet bills. It adapts to your needs.

4. Better utilization of your earnings

Without FBP, a large part of your salary goes into taxes. With FBP, that same money can be used for actual expenses.

5. Covers regular day-to-day costs

Expenses like meals, fuel, mobile bills, and learning courses can be included, reducing your personal spending.

6. Encourages financial discipline

Since you need to plan and submit bills, it helps you track where your money is going and manage it better.

7. Helps in long-term financial planning

By optimizing tax outflow, you can save more or invest more over time.

8. Flexibility to revise choices

In most companies, you can update your FBP declaration yearly based on changes in your lifestyle or expenses.

For Employers

1. Enhances employee satisfaction and engagement

When employees feel they have control over their salary structure, they are generally more satisfied and motivated.

2. Makes compensation packages more attractive

Even without increasing salaries, companies can offer better perceived value through flexible benefits.

3. Cost optimization without increasing CTC

Employers can design tax-efficient salary structures without increasing overall salary expenses.

4. Improves employee retention

Flexible benefits create a better employee experience, reducing the chances of attrition.

5. Ensures structured and transparent payroll

Clearly defined components make salary easier to understand and manage.

6. Better compliance and documentation

Since reimbursements require proof, it ensures proper record-keeping and reduces misuse.

7. Scalable and adaptable system

FBP policies can be adjusted based on company growth, employee needs, or tax changes.

Challenges Everyone Face in Flexible Benefit Plan (FBP)

While a Flexible Benefit Plan (FBP) helps in saving tax, it also comes with some practical challenges that employees should understand:

1. Can Be Confusing at First

Understanding different components, limits, and tax rules can be tricky, especially if you’re new to FBP.

2. Mandatory Bills and Documentation

To get tax benefits, you must submit proper bills (like fuel, phone, or meal expenses). Without proof, the amount becomes taxable.

3. Less Useful in New Tax Regim

Most FBP exemptions are not allowed in the new tax regime, so its tax-saving benefit becomes limited.

4. Incorrect Declaration Can Increase Tax

If you choose components that you don’t actually use or overestimate expenses, the unused amount gets taxed.

5. Strict Timelines to Follow

You need to declare FBP at the start and submit proofs on time. Missing deadlines means losing tax benefits.

Conclusion

A Flexible Benefit Plan (FBP) is more than just a salary component. It’s a smart way to optimize your income, reduce tax, and make better use of your earnings. By understanding the FBP full form, declaration process, and different allowances, you can take full control of how your salary works for you.

However, to get the maximum benefit, it’s important to declare your FBP correctly, choose the right components, and submit proofs on time. When used properly, FBP can significantly improve your take-home salary without increasing your CTC.

For organizations, managing FBP manually can be complex and time-consuming. This is where a smart solution like Savvy HRMS can help simplify the entire process, from easy declarations to smooth claim management and better compliance. Try Savvy HRMS to make FBP management effortless for both employees and employers.

Frequently Asked Questions

Is FBP part of salary or extra pay

FBP is generally part of your salary structure or CTC, not extra pay over and above it. The value comes from how salary is arranged, not from getting a second salary.

Can I claim FBP directly in my income tax return

The official salary-claim workflow is employer-facing: claims, exemptions, allowances, and evidence are furnished to the employer so TDS can be computed correctly. The return is important, but it does not replace the employer-side declaration process.

Is HRA part of FBP

It can be, depending on employer policy. Where HRA is part of salary, the official exemption formula applies under the old regime rules, but the HRA exemption is not available in the new regime.

Does FBP work better in the old regime or new regime

In many practical cases, FBP is more useful when old-regime-style exemptions are relevant, because the new regime allows far fewer exemptions and deductions. But the official advice is still to compare both regimes before deciding.

What documents are usually needed

That depends on the component and your employer policy, but official salary-claim forms make it clear that evidence or particulars of the claim are furnished to the employer for tax deduction purposes.