Ever looked at your salary slip at the end of the month and wondered, “I earn this much, so why am I paying so much tax?” Well, you are not alone. Millions of salaried employees across India find themselves confused about what portion of their income is actually taxable and what’s not.

Here’s the good news: understanding how to calculate taxable income isn’t as complicated as it sounds. Once you know how the system works, you can plan smarter, save more, and avoid unnecessary surprises during tax season.

Whether you are a fresher filing your first return or a seasoned professional trying to optimise deductions, this guide breaks down the computation of taxable income in plain and simple language, no jargon, no confusion.

What Is Taxable Income?

Simply put, taxable income is the portion of your earnings on which you are required to pay income tax to the government. It is not your entire salary; rather, it’s what remains after you subtract all the eligible exemptions, allowances, and deductions from your gross income.

Think of it this way: your employer pays you a certain amount, but the government only taxes a part of it, the part that doesn’t qualify for any tax relief under the Income Tax Act, 1961.

Your taxable income in India can come from multiple sources, such as salary, house property, business or profession, capital gains, and other sources. For salaried employees, the primary source is their employment income, but other incomes like interest on savings, rent received, or capital gains may also be added to arrive at the final taxable figure.

Difference Between Gross Income and Net Taxable Income

| Parameter | Gross Income | Net Taxable Income |

| Definition | Total income earned before any deductions or exemptions | Income remaining after subtracting all exemptions and deductions from gross income |

| Also Known As | Gross Total Income (GTI) | Total Taxable Income |

| What It Includes | Basic salary, HRA, allowances, bonuses, DA, rental income, interest, dividends, capital gains | Gross income minus all eligible exemptions, deductions & allowances |

| Exemptions Applied? | ❌ No | ✅ Yes |

| Deductions Applied? | ❌ No | ✅ Yes (80C, 80D, 80CCD, etc.) |

| Standard Deduction | Not yet applied | Already deducted (₹75,000 for salaried) |

| HRA Exemption | Not yet applied | Already deducted |

| Used For | Understanding total earnings | Calculating actual tax liability |

| Tax Calculated On? | ❌ No | ✅ Yes, this is what gets matched against the tax slab |

| Example Amount | ₹12,00,000 | ₹8,60,000 (after all deductions) |

| ITR Reference | Shown as Gross Total Income in ITR | Shown as Total Income / Net Taxable Income in ITR |

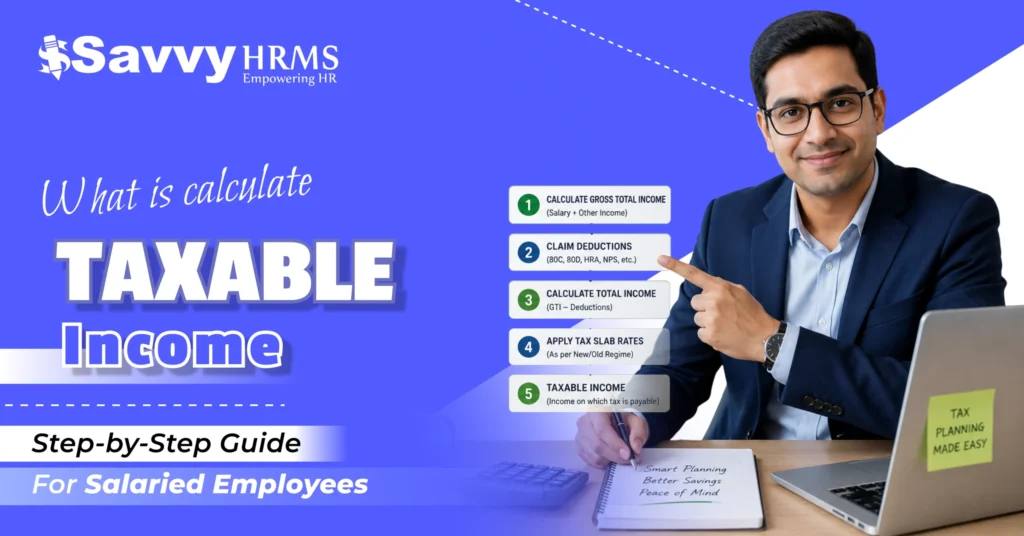

How to Calculate Taxable Income?

This is the heart of the matter. Let’s walk through how to calculate taxable income from salary in a structured, step-by-step manner.

Step 1: Start with Your Gross Salary

Begin with your Cost to Company (CTC) or gross salary. This includes:

- Basic Salary

- Dearness Allowance (DA)

- House Rent Allowance (HRA)

- Special Allowances

- Bonus and incentives

- Leave Travel Allowance (LTA)

- Any other perquisites

Step 2: Subtract Exemptions from Allowances

Certain allowances are partially or fully exempt from tax. Key exemptions include:

- HRA Exemption: Calculated based on actual HRA received, rent paid, and city of residence (metro vs non-metro). The least of the three applicable values is exempt.

- LTA Exemption: Exempt for actual travel expenses within India, twice in a block of four years.

- Children’s Education Allowance: Up to ₹100 per month per child (max 2 children).

- Standard Deduction: A flat deduction of ₹75,000 is available to all salaried employees under the new tax regime (FY 2025-26 onwards).

Step 3: Calculate Income from Salary (After Exemptions)

Once you subtract the allowance exemptions from gross salary, you arrive at your net salary income, which forms the primary component of your taxable income.

Step 4: Add Income from Other Sources

This is where many salaried employees miss out. Your total taxable income isn’t just your salary; it includes other income as well:

- Interest income from savings accounts, FDs

- Rental income from house property

- Capital gains from mutual funds, shares, or property

- Freelancing or side business income

Is dividend income taxable?

Yes! Since the ending of the Dividend Distribution Tax (DDT) in 2020, dividend income is fully taxable in the hands of the recipient at their applicable slab rate. If your dividend income exceeds ₹5,000 in a year, TDS at 10% is also applicable. So if you are an investor receiving dividends from stocks or mutual funds, make sure to include this in your total taxable income.

Is agricultural income taxable?

Agricultural income is exempt from income tax under Section 10(1) of the Income Tax Act. However, if you have non-agricultural income exceeding the basic exemption limit, your agricultural income is used to determine the applicable tax slab rate (partial integration method). So while the agricultural income itself isn’t directly taxed, it can push your other income into a higher tax bracket.

Step 5: Subtract Deductions Under Chapter VI-A (Old Regime)

If you opt for the old tax regime, you can claim a range of deductions:

- Section 80C: Up to ₹1.5 lakh (PPF, ELSS, LIC, EPF, NSC, home loan principal, etc.)

- Section 80D: Health insurance premiums (up to ₹25,000 for self/family; ₹50,000 for senior citizens)

- Section 80CCD(1B): Additional ₹50,000 for NPS contribution

- Section 24(b): Interest on home loan up to ₹2 lakh (self-occupied property)

- Section 80E: Interest on education loan (no upper limit)

- Section 80TTA/80TTB: Interest on savings account (₹10,000 for individuals; ₹50,000 for senior citizens)

Note: Under the new tax regime, most of these deductions are not available. However, the standard deduction of ₹75,000 and the employer’s NPS contribution deduction under Section 80CCD(2) are still allowed.

Step 6: Arrive at Your Net Taxable Income

| Net Taxable Income = Gross Salary + Other Income − Exemptions − Deductions |

This final figure is what gets matched against the taxable income slab to determine how much tax you owe.

How to Calculate Taxable Income in India? A Quick Example

Let’s say Riya earns a gross salary of ₹12,00,000 per year:

| Particulars | Amount (₹) |

| Gross Salary | 12,00,000 |

| Less: HRA Exemption | (1,20,000) |

| Less: Standard Deduction | (75,000) |

| Net Salary Income | 10,05,000 |

| Add: Interest Income (FD) | 30,000 |

| Gross Total Income | 10,35,000 |

| Less: 80C Deductions | (1,50,000) |

| Less: 80D (Health Insurance) | (25,000) |

| Net Taxable Income | 8,60,000 |

Types of Income That Are Taxable

Under the Income Tax Act, income is classified under five heads:

1. Income from Salary

Any income received from an employer, including basic wages, pension, bonuses, gratuity, and perquisites, falls under this head and is taxable.

2. Income from House Property

Rental income from any owned property is taxable. Even a self-occupied home can attract notional rent tax in specific situations.

3. Income from Business or Profession

Net profits earned through running a business, freelancing, or professional consultancy are fully taxable under this head after allowable expense deductions.

4. Income from Capital Gains

Profit from selling assets, stocks, mutual funds, gold, or real estate is taxable as either Short-Term or Long-Term Capital Gains, accordingly.

5. Income from Other Sources

A residual catch-all head covering all income not classified elsewhere. It includes:

- Interest from Savings & FDs

- Dividend Income

- Lottery or Game Show Winnings

- Gifts Exceeding ₹50,000

- Family Pension

Tax Slabs for FY 2026-27 (AY 2027-28)

New Tax Regime

The new tax regime is now the default regime in India. It offers lower tax rates but fewer deductions.

| Taxable Income Slab | Tax Rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% and above |

- Tax Rebate under Section 87A: Individuals with net taxable income up to ₹12,00,000 get a full tax rebate under the new regime (i.e., zero tax payable). The standard deduction of ₹75,000 means salaried employees with income up to ₹12,75,000 effectively pay zero tax.

- Surcharge: Applicable on tax amount for income above ₹50 lakh – 10% (₹50L–₹1Cr), 15% (₹1Cr–₹2Cr), 25% (₹2Cr–₹5Cr), 25% (above ₹5Cr under new regime).

- Health & Education Cess: 4% on total tax + surcharge.

Old Tax Regime

| Taxable Income Slab | Tax Rate |

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Under the old regime, the Section 87A rebate is available for income up to ₹5,00,000 (tax rebate up to ₹12,500).

Source: https://www.incometax.gov.in/

Conclusion

Understanding your taxable income in India is not a one-time activity; it’s a habit that pays off every year. When you know exactly how much of your salary is taxable and which deductions you’re entitled to, you stop overpaying taxes and start making smarter financial decisions throughout the year.

Getting your computation of taxable income format right also helps you file your ITR accurately and on time, avoiding penalties, notices, and last-minute stress. Whether you choose the new tax regime or stick with the old one, the key is to plan ahead and keep your income and investment documents organised and up to date. That’s exactly where Savvy HRMS steps in. From automated salary structuring and HRA calculations to TDS management and Form 16 generation, Savvy HRMS takes the complexity out of payroll and tax compliance, so your HR team spends less time on spreadsheets and more time on what actually matters. Smart payroll is just a few clicks away.

Ready to simplify your salary and tax calculations?

Get started with Savvy HRMS today, because your payroll shouldn’t be a puzzle.

Book a Demo Today